Opportunities for OTT in LATAM are improving year on year, but there are changes underway as the market reacts to the presence of greater competition.

It has been a busy few years in the LATAM video industry, with the result being various changes across the industry’ regional landscape. For starters, major new entrants have launched in the region, operating across several diverse markets, resulting in consumers having more choice than ever before.

It has been a busy few years in the LATAM video industry, with the result being various changes across the industry’ regional landscape. For starters, major new entrants have launched in the region, operating across several diverse markets, resulting in consumers having more choice than ever before.

With that in mind, we thought we would highlight some of the directions the market is heading in, as well as some of the reasons why it is changing, and where it might be going in the near future.

The top trends in LATAM OTT

Without doubt the biggest trend in LATAM at the moment is Super Aggregation. It is a subject foremost in many minds, and we are also seeing a large amount of queries relating to the technologies that underpin it, such as universal search, effective content hubs, and the increasing use of data analytics.

We are also seeing a wholesale move from Linux-based STBs to Android TV powered ones. This is accompanied by a realisation amongst many operators that the future of the industry is app-based, and they are rapidly pivoting towards establishing an ecosystem that reflects that.

The overall picture of OTT

One of the biggest changes in the region came at the end of 2021, when three major American studios launched their platforms. Disney+ & Star+ (Walt Disney Company), HBO Max (Warner Media Discovery), and Paramount+ (Viacom) all entered the Latin-American market, joining the historical leader, Netflix, and Amazon Prime Video. These five major regional players are surrounded by many smaller scale competitors that either concentrate on local offerings or niche content.

As Dataxis notes, the outcome has been an increase in service stacking. By Q2 2022, there were more than 90 million OTT SVOD accounts in the region, which works out as an average of 1.8 services per household. This figure evidently keeps growing as well, with an average of 1.5 services per household in 2021, and only 1.2 services per household, in 2020.

Will it break the two services per household barrier in 2023? It is possible. The three new entrants have certainly made an impact, Dataxis figures again suggesting that they captured a 35% market share in just four quarters. Netflix has been the main company to lose out, losing 30 points of market share as a result (though this may also be tied into its experiments in the region with rolling out account sharing ban - see below).

With regard to our previous mention of Super Aggregation, one interesting thing to note is that the new entrants in particular have widened the scope of strategic alliances to include other industries. From a historical base of OTT being provided by telcos and Pay TV operators, the list of providers now includes banks, credit cards, airlines, and retailers. OTT is therefore no longer solely positioned as adding value to a telecommunications product in a triple or quad-play, but is increasingly seen as a powerful element in the loyalty programs of other industries. Consequently the big five players have established ties with 81 regional companies, as per Dataxis.

Monthly ARPU across the region is comparatively low at $6 per user, but revenues are still increasing. Digital TV Research sees them doubling to $14bn by 2027 with SVOD subscriptions increasing to 145 million. If this growth holds true to its projections, it will see the number of services per household rise up to roughly 2.9.

Video piracy in LATAM

Netflix chose to trial its initiatives to move customers from password sharing to paid sharing in Latin America during 2022, starting with Chile, Costa Rica, and Peru before widening it out to other countries in the region. It refined it considerably during the tests, discarding one initial model of allowing users to add another household in favour of one that lets them add individual members instead.

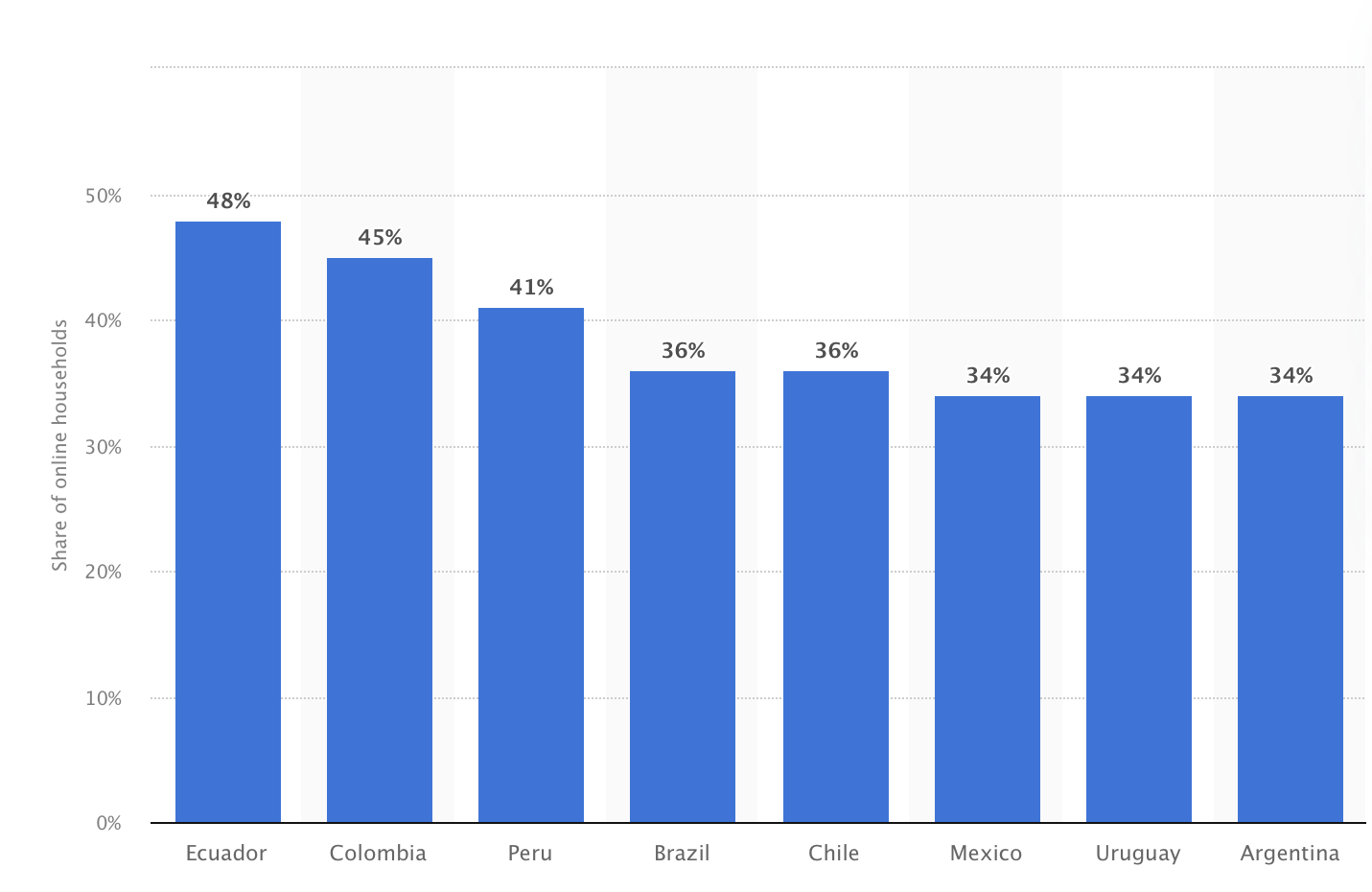

Unfortunately, LATAM is a good region for such testing to take place as piracy levels remain high. Figures from one recent quarter show that approximately 48% of households with access to the internet in Ecuador consumed pirated online videos. This is followed by Colombia with a figure of 45%, before declining to 34% in Argentina, Mexico, and Uruguay.

Source: Statista

One of the issues is that each country has its own individual laws and legislative framework for dealing with online video piracy. As a result, we are starting to see action being taken by regional trade bodies. For example, CERTAL, the Center for Studies for the Development of Telecommunications and Access to the Information Society of Latin America, announced the signing of a new Global Anti-Piracy Pact (Pacto Global Antipirateria), by more than twenty public and private companies from the region. Amongst other initiatives, this mandates the implementation of mandatory forensic watermarking in video content as well as creating “entities specialized in anti-piracy matters.”

The entire industry will hope that it has an impact.

2023: an exciting year for LATAM OTT

At the end of last year, we gathered our regional experts together and asked them how they thought that 2023 would shape up for operators around the world. There were many fascinating responses as each talked about their own territories and the forces being applied on them.

The good news is that business confidence is high. Together we scored our optimism for 2023 at 7.9 out of 10, with LATAM being one of several that scored 8 out of 10.

It will, of course, be an interesting year with many challenges. But there is cause for much optimism. Consumers are becoming used to managing a larger stack of streaming services, and those services in turn are pivoting into a more flexible app-based future. And with the Big 5 American studios increasingly localizing their offerings while niche players successfully build audiences, 2023 looks set to be an exciting year as well.

.jpeg)